Lesson of the Day: Financial Theory of Inflation's Effects on Real Assets

Contents

About the Author

Learn about our Refer-a-Friend Program. Terms and conditions apply.

Financial theory says that when there is unexpected inflation, monetary assets (things that use dollars to satisfy contractual obligations, such as bonds, loans, and cash) are going to decline in value. The theory also states that non-monetary assets (such as stocks and real estate) will not be affected in the long-run.

In this lesson, let's focus on stocks. The stock certificate does not say "you get "X" amount of dollars over "X" amount of time" like bonds do. The certificate simply states you get a percentage of the company's net profit. For instance, with stock ownership, if a company sells $100 worth of product, and after expenses of $90, the company earns $10 which is yours to keep. If, due to 10% inflation, that company is now able to charge $110, and after expenses of $99 (since expenses go up 10% also) you now earn $11, which is 10% more than before.

Theoretically, stock owners are not hurt by inflation since when their profit goes up, so do their dividends, which is followed by an increase in their stock price.

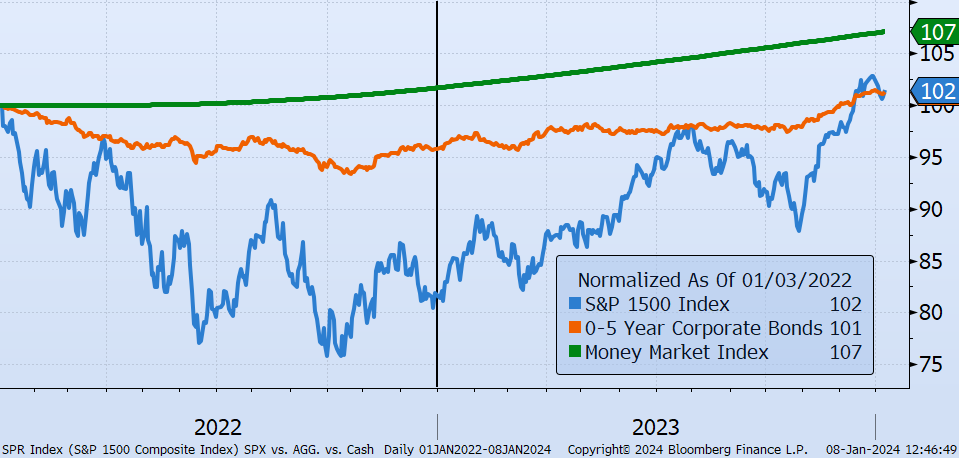

The issue is in the short-term. Often, assets will decline in value due to higher discount rates and quite simply because it takes time for companies to raise their prices and to realize higher profits. This is the phenomenon that was experienced during the recent inflation spike, which caused short-term stock price declines in 2022. However, as companies were able to “adjust” we saw their recovery in 2023.

Sadly, monetary assets, such as bonds, do not get this option as they are locked into the terms originally agreed upon until the contract is over (a.k.a the maturity date). However, since they are contractually obligated, their value does not vary as much as stocks which have no such conditions.

Depending on individual circumstances, an allocation to both stocks and bonds can be good for a portfolio, but financial theory states that in the long-term stocks and things like real estate are the best ways to help stay ahead of inflation.

Samuel serves as Senior Vice President, Chief Investment Officer for the Crews family of banks. He manages the individual investment holdings of his clients, including individuals, families, foundations, and institutions throughout the State of Florida. Samuel has been involved in banking since 1996 and has more than 20 years experience working in wealth management.

Investments are not a deposit or other obligation of, or guaranteed by, the bank, are not FDIC insured, not insured by any federal government agency, and are subject to investment risks, including possible loss of principal.