Overdraft Coverage Options

Overdraft Protection and Overdraft Privilege for Your Business

Life happens! At Crews Bank & Trust, we understand that from time to time you may unexpectedly overdraft your account. Returned checks can be costly, but you have options for covering unexpected overdrafts. Overdraft Coverage can help.

Consider these ways to cover overdrafts:

Establish Overdraft Protection.

This is your least costly way to cover overdrafts. With this option, overdrafts will be transferred and there is a $3 OD Sweep Fee (per transfer) for the transfer to cover the overdraft. You simply link your Business Checking account to another deposit account you have with us. Call us at 888-406-2220, email us at support@crews.bank, or come by a branch to sign up or apply for this service.

Utilize your Overdraft Privilege.

This service lets you overdraft your account up to the disclosed limit for a $33 per Overdraft Item Fee to pay for the transaction. Even if you have Overdraft Protection, Overdraft Privilege is available as secondary coverage if the other protection is exhausted.

All eligible business accounts have Extended Overdraft Privilege Coverage, which covers all transaction types listed below:

What Else You Should Know

Linking your checking account to another deposit account may be a more cost-effective option than an overdraft. You must sign up for this service, and there is a $3 fee per transfer to cover the overdraft.

A single larger overdraft will incur just one fee, unlike multiple smaller overdrafts which can result in multiple fees. Good account management is the best way to avoid overdrafts. Use our mobile banking, online banking, and telephone banking services to monitor your balance. For additional financial education resources, please visit www.mymoney.gov.

The $33 Overdraft Item Fee charged for overdrawing your account is the same fee applied if an item is returned unpaid. If multiple items overdraw your account on the same day, each item will incur an Overdraft Item Fee or a Return Item Fee of $33. All fees and charges are included as part of the Overdraft Privilege limit amount. Your account may become overdrawn beyond the Overdraft Privilege limit due to these fees.

Recipients of federal or state benefits who do not want us to deduct the overdrawn amount and the Overdraft Item Fee from their deposits can call us at 888-406-2220 to discontinue Overdraft Privilege.

If an item is returned because your Available Balance (as defined below) is insufficient, and the item is presented for payment again, Crews Bank & Trust (“We”) may charge a Returned Item Fee each time the item is returned. This means you could be charged more than one fee for any given item if it is returned and represented. When we charge a Return Item Fee, it reduces your Available Balance and may put your account further into overdraft. If, upon representment, the Available Balance is sufficient to cover the item, we may pay it and, if this causes an overdraft, charge an Overdraft Item Fee.

We may use the terms “item” and “transaction” interchangeably.

For consumer accounts, we limit Overdraft Item Fees to $165 (5 fees) per day. We do not charge an Overdraft Item Fee if a consumer account is overdrawn by $10 or less. These exceptions do not apply to business accounts.

Here is how we determine overdrafts: We generally post transactions throughout the day, credit before debits. If there are available funds to cover some, but not all, of the withdrawals or other debits to your account on a single business day, we will post the checks for which there are sufficient available funds in sequential order by check number, from the lowest check to the highest. ATM, debit card, and ACH transactions are each posted from lowest to highest dollar amount within their category, in the order of ATM first, then debit card, then ACH transactions. However, due to the various ways you can access your account, the posting order of individual items may differ from these general policies. Holds on funds and the order in which transactions are posted can impact the total amount of Overdraft Item Fees or Return Item Fees assessed.

We may be required to pay some debit card transactions that are not authorized through the payment system due to payment system rules, which could result in fees if such transactions overdraw your account. However, we will not authorize debit card or ATM transactions unless your account’s Available Balance (including Overdraft Coverage Options) is sufficient to cover the transactions and any associated fees.

By giving us your consent to pay everyday debit card and ATM overdrafts on your consumer account (Extended Coverage), you may incur Overdraft Item Fees for transactions that we would otherwise be required to pay without assessing a fee. However, this consent allows us to authorize transactions up to the amount of your Overdraft Privilege limit. If you consent to Extended Coverage, it will remain on your account until you withdraw it.

Overdraft Privilege is not a line of credit; it is a discretionary service that can be withdrawn at any time without prior notice. The depositor and each authorized signatory are jointly and severally liable for all overdraft and fee amounts, as described in the Account Agreement. The total negative balance, including all fees and charges, is due and payable upon demand.

Understanding Your Available Balance

Your account has two types of balances: the Ledger Balance and the Available Balance. We use the Available Balance to authorize and pay transactions.

- Ledger Balance: This reflects the full amount of all deposits to your account and all posted payment transactions. It does not include checks you have written that are still outstanding or transactions that have been authorized but are still pending.

- Available Balance: This is the amount you can use for purchases, withdrawals, or to cover transactions. It is your Ledger Balance minus any holds due to pending debit card transactions and holds on deposited funds.

Authorization of Transactions:

- For checks, ACH items, and recurring debit card transactions, the balance used is your Available Balance plus the Overdraft Privilege limit and any available Overdraft Protection.

- For ATM and everyday debit card transactions with Standard Coverage, the balance used is your Available Balance plus any available Overdraft Protection, but it does not include the Overdraft Privilege limit.

- For ATM and everyday debit card transactions with Extended Coverage, the balance used is your Available Balance plus any available Overdraft Protection and includes the Overdraft Privilege limit.

Important Points:

- Your Available Balance reflects pending transactions and debit holds, so it may appear sufficient to cover a transaction, but upon settlement, it might not be. This could result in further overdrawing your account and additional overdraft fees.

- Any item that would overdraw your account based on your Available Balance may create an overdraft.

- We may place a hold on deposited funds according to our Account Agreement, reducing your Available Balance.

- The Overdraft Privilege amount is not included in the available balance shown through online banking, mobile banking, or Crews Bank & Trust ATMs.

- We will place a hold on your account for any authorized debit card transaction until it settles (usually within two business days) or as permitted by payment system rules. Sometimes, the hold may exceed the transaction amount. When the hold ends, the funds will be added to your Available Balance. If your account is overdrawn after the held funds are added and the transaction is posted, an Overdraft Item Fee may be assessed.

- Except as described here, we will not pay items if your Available Balance (including the Overdraft Privilege limit, if applicable) is insufficient to cover the items and any fees.

Debit Card Suspension:

- If your account is overdrawn for more than 32 consecutive days, your debit card(s) may be suspended. They will remain suspended until you make sufficient deposits to bring your account balance to a positive status.

- If your debit card is suspended, you will not be able to use it for purchases or ATM access. If you use your debit card for recurring payments, such as utilities, we encourage you to arrange alternative payment methods to avoid interruptions.

Understanding Overdraft Privilege Limits

At account opening, Eligible Consumer Checking accounts will receive an Overdraft Privilege limit of $500 while eligible Business Checking accounts will receive a limit of $1,000. Overdraft Privilege may be suspended if you default on any loan or other obligation to us, or if your account becomes subject to any legal or administrative order or levy. If you do not maintain your account in good standing by bringing it to a positive balance within 32 days for at least one business day, your Overdraft Privilege limit may be reduced. To reinstate the full Overdraft Privilege limit, you must bring your account balance to a positive status for at least one business day.

If you have any questions about Overdraft Protection or Overdraft Privilege, please email us at support@crews.bank, call us at 888-406-2220, or visit a branch.

Blog

On Our Minds

10 Estate Planning Errors That Cost Time, Money, and Your Sanity

April 23, 2025

Estate planning often gets put on the back burner. Like the all-too-familiar ritual of tax filing procrastination, many of us recognize its...

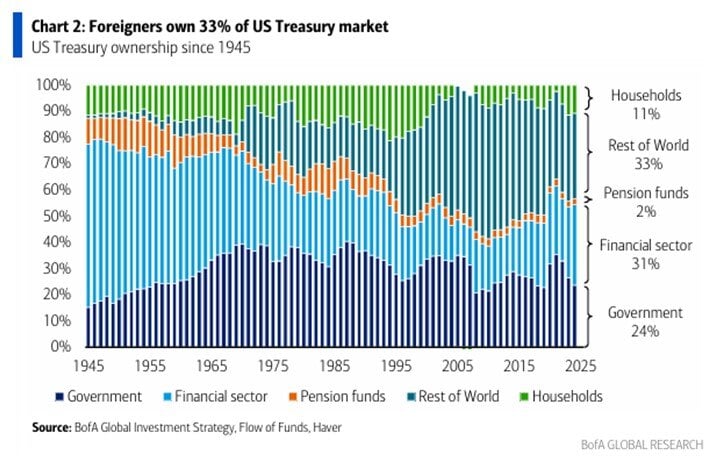

Chart of the Day: Who Do We Owe?

April 22, 2025

Today’s Chart of the Day from BofA Global Research shows the percentages of US treasury bond ownership spanning from 1945 to 2025.

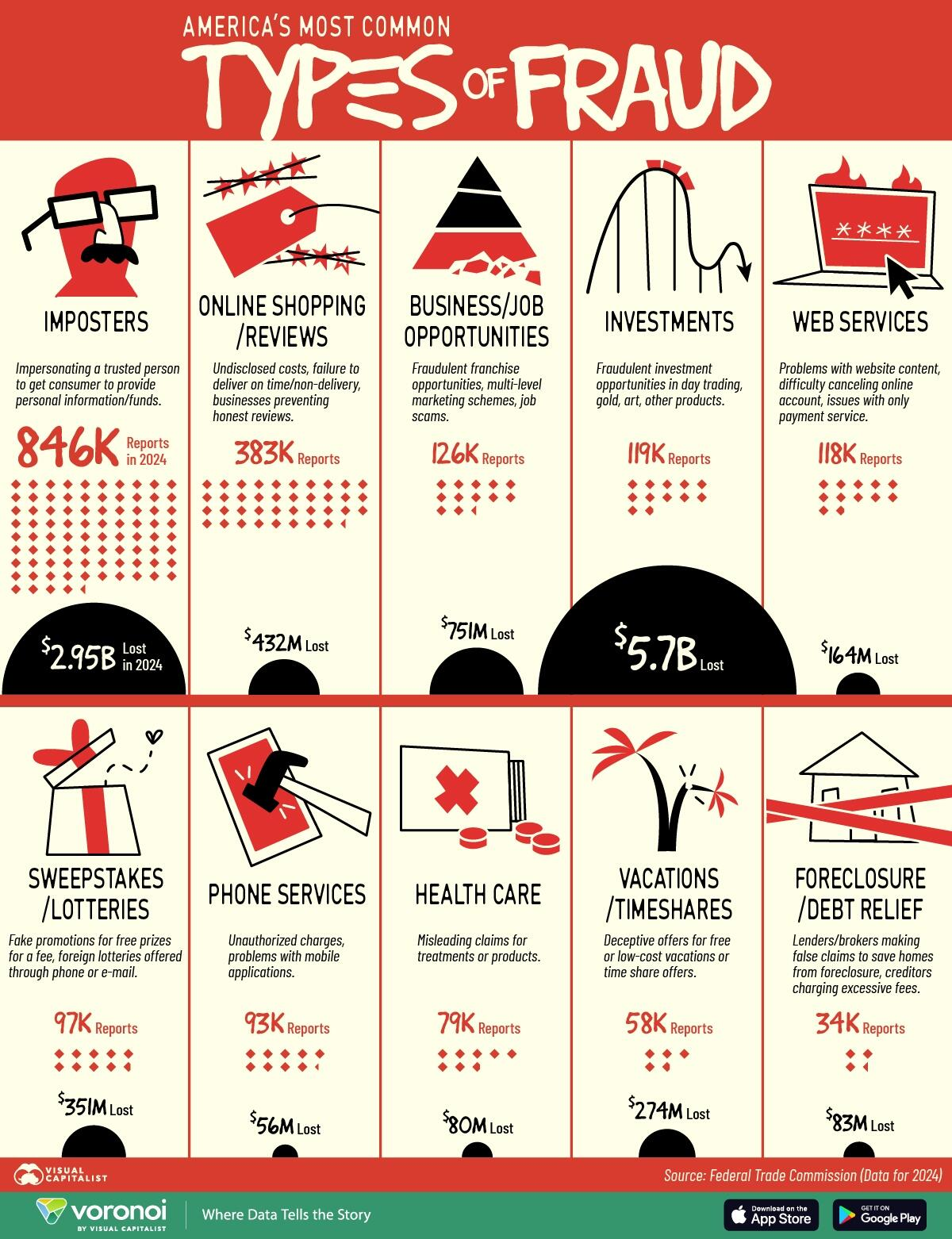

Chart of the Day: Types of Fraud

April 17, 2025

Today’s Chart of the Day is from Visual Capitalist detailing and ranking common types of fraud. The report suggests losses are half a trillion...