Chart of the Day: Don't Feel Too Bad

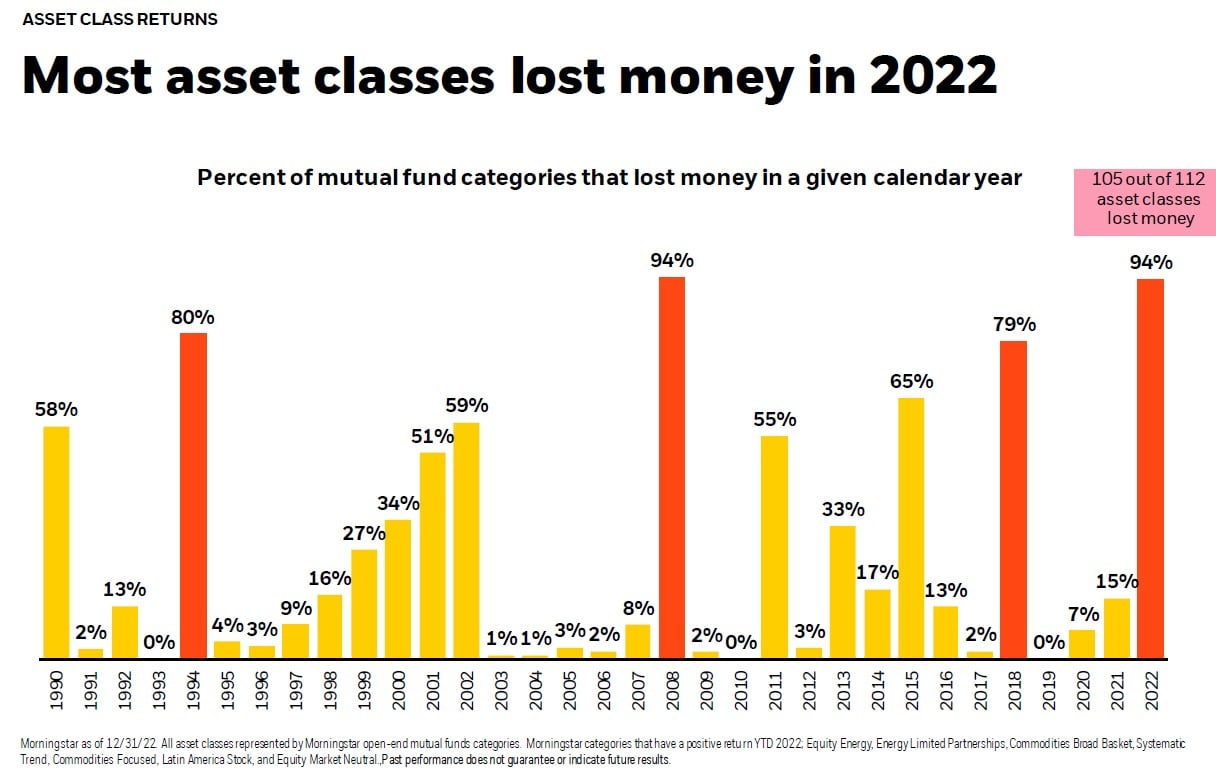

Today’s Chart of the Day comes from BlackRock and shows that 105 of 112 asset classes lost money in 2022.

Today’s Chart of the Day comes from BlackRock and shows that 105 of 112 asset classes lost money in 2022.

As a family-owned and operated bank, we pride ourselves on serving the individuals, families, and businesses of Florida by providing premier banking..

As our communities continue to recover from recent hurricanes, and with everyone knee deep in tax season, we are updating a blog from December with..

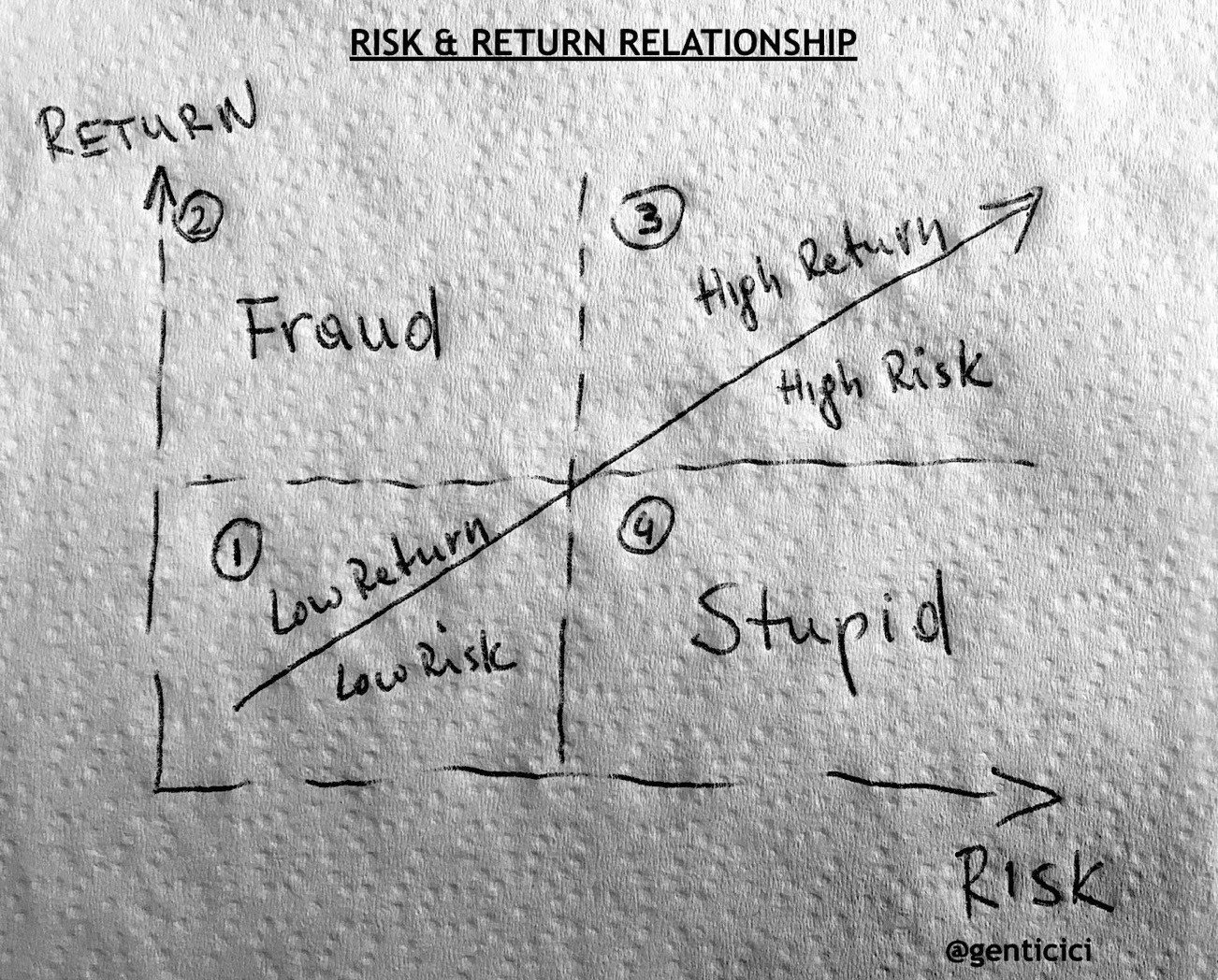

Today’s Chart of the Day comes from @genticici on Twitter. I was impressed by the simplicity of the concept, and it's very apropos to be on the back..

Today’s Chart of the Day is a reoccurring one we like to keep updated with current data.

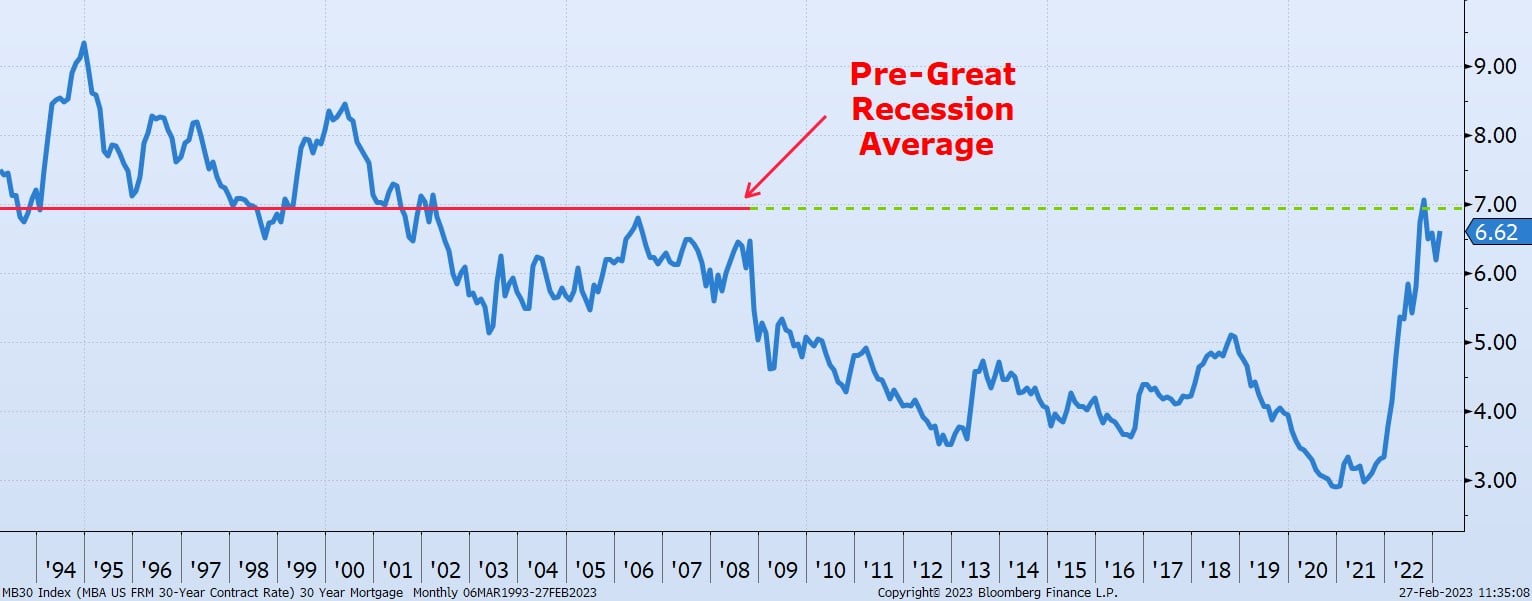

Today's Chart of the Day, compiled from information from the Mortgage Bankers Association, shows the 30-year residential rates dating back to 1993.

The time of low-cost debt has finally come to an end. With skyrocketing rates in 2022 to combat inflation, combined with global financial uncertainty..

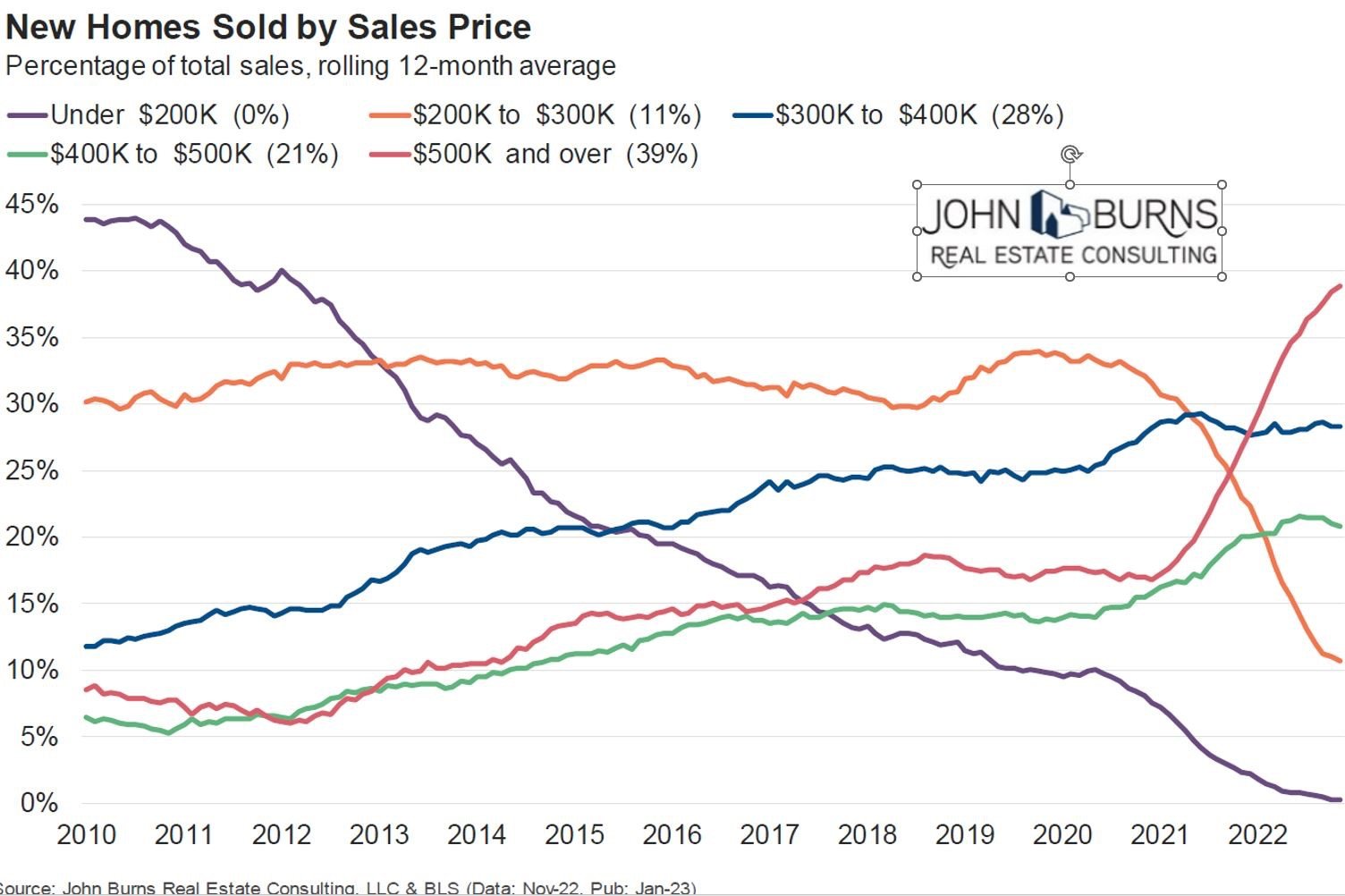

Today’s Chart of the Day comes from John Burns and shows the historical percentages of homes sold by sales price going back to 2010.

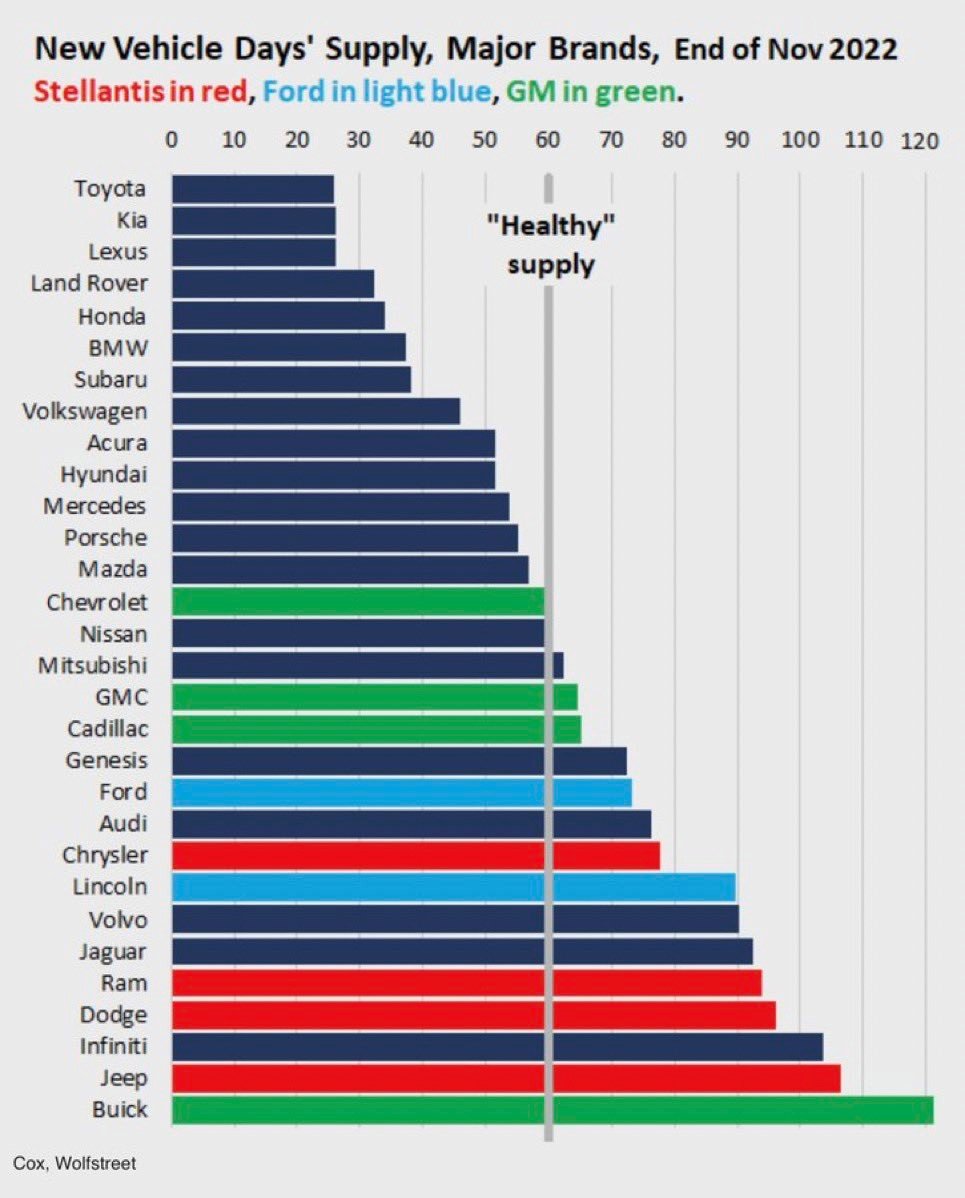

Today’s Chart of the Day comes from Wolfstreet and shows the supply of new vehicles in number of days.

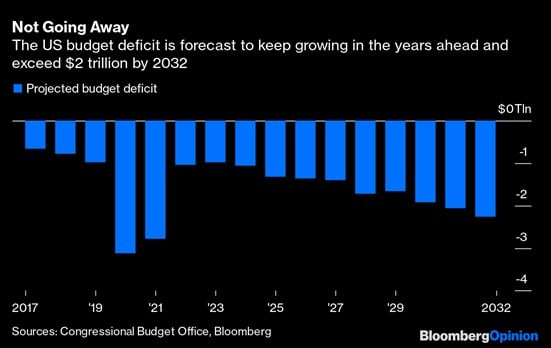

Today’s Chart of the Day is the projected budget deficits for the next 10 years provided by the Congressional Budget Office. It is not a rosy picture.

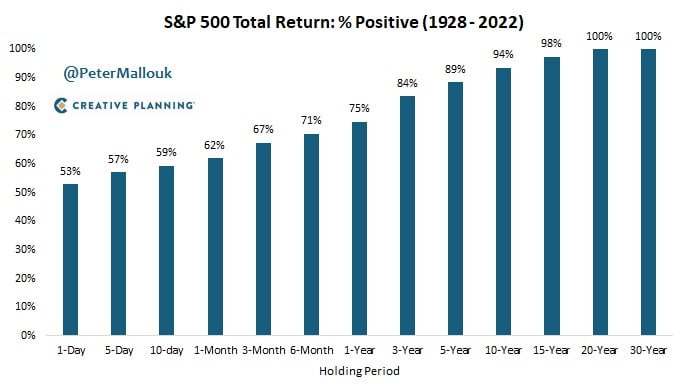

Today’s Chart of the Day comes from @PeterMallouk on Twitter and shows the percent of time the S&P 500 is positive, depending on your holding period,..

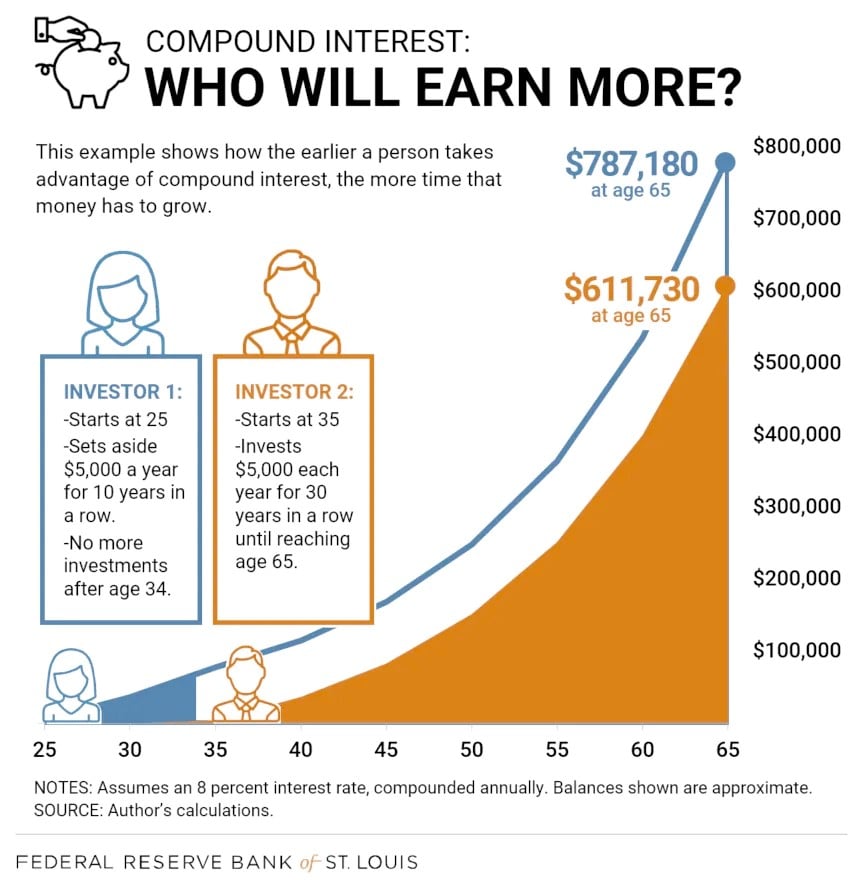

Today’s Chart of the Day is from the Federal Reserve Bank of St. Louis supporting the mantra, "Save early, Save often."

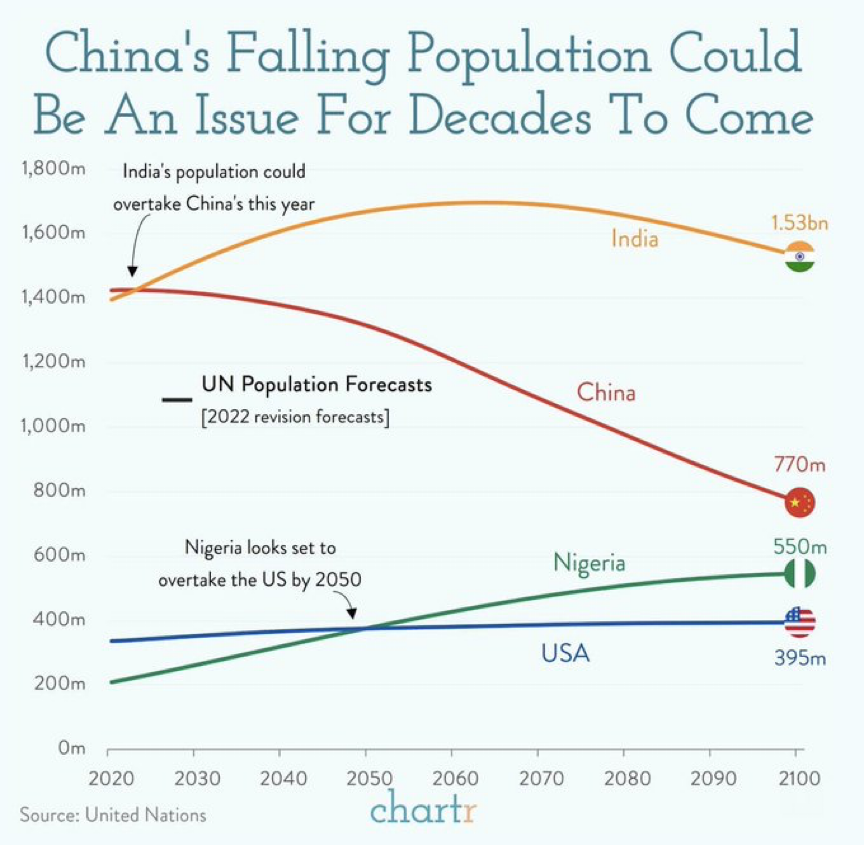

Today’s Chart of the Day comes from chartr with data provided by the United Nations.

Whether it’s fear of thinking about the end of life or they just don’t believe they have enough money and assets to worry about, only 33% of American..

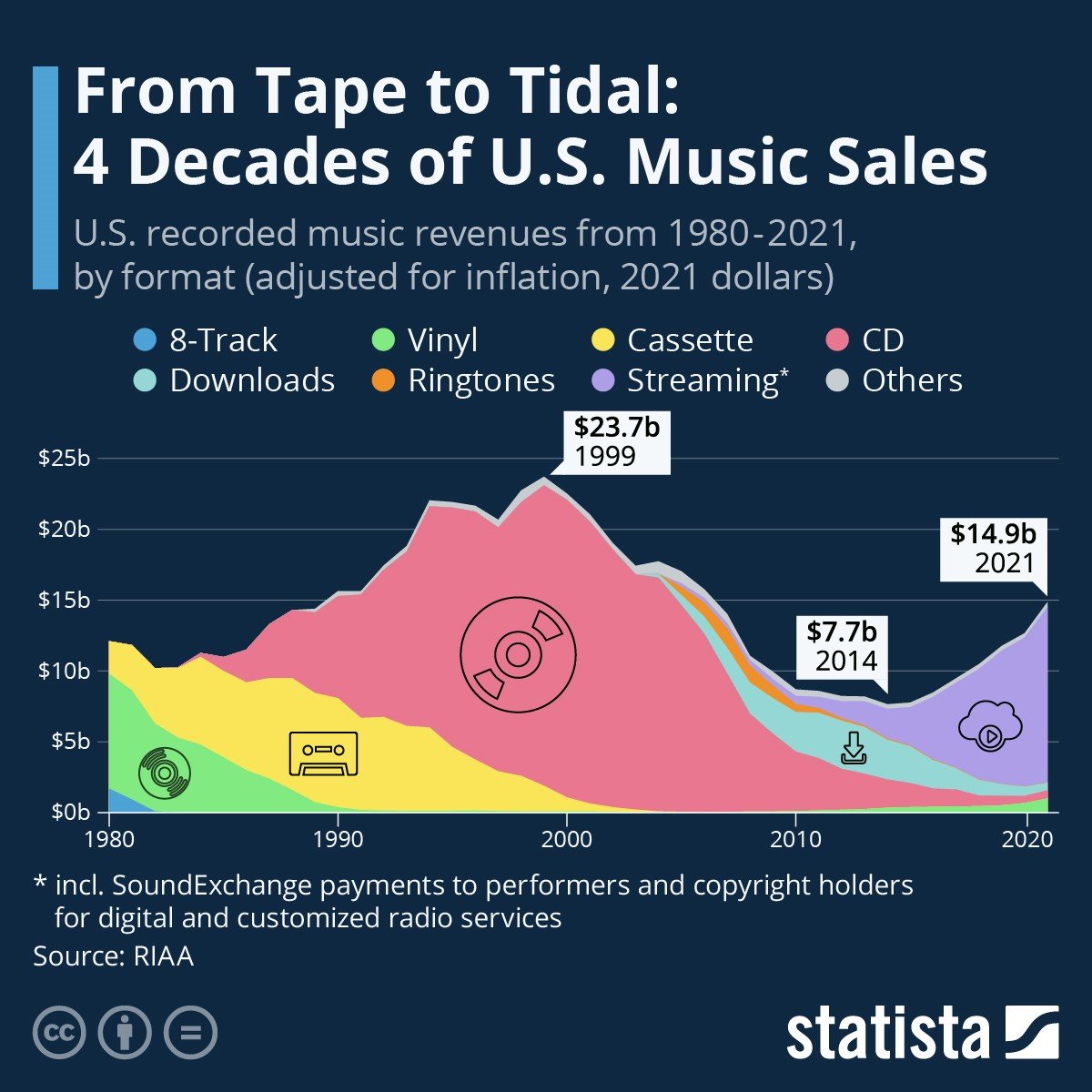

Today’s Chart of the Day comes from Statista, a provider of market and consumer data. The chart shows that streaming music, purple, has taken over..